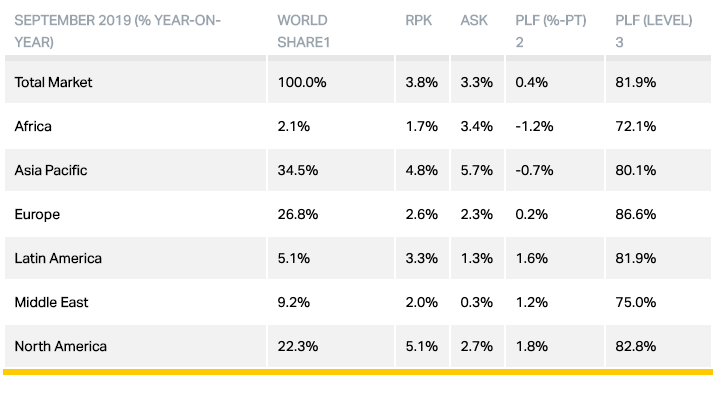

Geneva – The International Air Transport Association (IATA) announced global passenger traffic results for September 2019 showing that demand (measured in revenue passenger kilometers or RPKs) climbed 3.8% compared to the same month last year, broadly unchanged from August’s performance. Capacity (available seat kilometers or ASKs) increased by 3.3%, and load factor climbed 0.4 percentage point to 81.9%, which was a record for any September.

«September marked the eighth consecutive month of below average demand growth. Given the environment of declining world trade activity and tariff wars, rising political and geopolitical tensions and a slowing global economy, it is difficult to see the trend reversing in the near term,» said Alexandre de Juniac, IATA’s Director General and CEO.

International Passenger Markets

September international passenger demand rose 3.0%, compared to September 2018, which was a decline from 3.6% year-over-year growth achieved in August. All regions recorded traffic increases, led by airlines in North America. Capacity climbed 2.6%, and load factor edged up 0.3 percentage point to 81.6%.

Asia-Pacific airlines saw September traffic increase 3.6% compared to the year-ago period, an increase over the 3.3% annual growth recorded in August. Despite the uptick, growth remains well below that seen in 2018. This is occurring amid a weaker economic backdrop in some of the region’s key states as well as trade tensions between the US and China and, more recently, between Japan and South Korea. Political unrest in Hong Kong has also contributed to subdued regional demand and led to sharp capacity cuts to/from the hub. Capacity rose 5.0% and load factor slid 1.1 percentage points to 78.2%.

European carriers experienced a 2.9% rise in September traffic, the region’s weakest performance this year and a decline from the 4.2% year-over-year rise recorded in August. In addition to slowing economic activity and faltering business confidence in many of the key European economies, the result was also affected by the demise of a number of airlines, along with pilot strikes. Capacity rose 2.5%, and load factor climbed 0.3 percentage point to 86.9%, which was the highest among regions.

Middle Eastern airlines posted a 1.8% traffic increase in September, which was a slowdown from a 2.9% rise in August. Capacity was up just 0.2%, with load factor climbing 1.2 percentage points to 75.2%. International traffic growth continues to be affected by a mix of structural challenges in some of the region’s large airlines, geopolitical risks and weaker business confidence in some countries.

North American carriers’ international demand climbed 4.3% compared to September 2018, well up from the 2.9% growth recorded in August and the strongest performance among the regions. Capacity rose 1.6%, and load factor accelerated 2.2 percentage points to 83.0%. Demand is being supported by solid consumer spending and continued job creation.

Latin American airlines had a 1.2% demand increase in September compared to a year ago, which was down from 2.3% growth in August. Capacity fell 1.6% and load factor surged 2.3 percentage points to 82.5%. Latin American carriers continue to face several challenges including some weaker economic and business confidence outcomes, political and social unrest in key states, and currency exposure to the strengthening US dollar.

African airlines’ traffic climbed 0.9% in September, a steep fall-off from the 4.1% growth recorded in August. Looking through the recent volatility in the numbers, however, traffic growth for the third quarter of 2019 remains solid at around 3% year-over-year. Capacity rose 2.5%, however, and load factor dipped 1.1 percentage points to 71.7%.

Domestic Passenger Markets

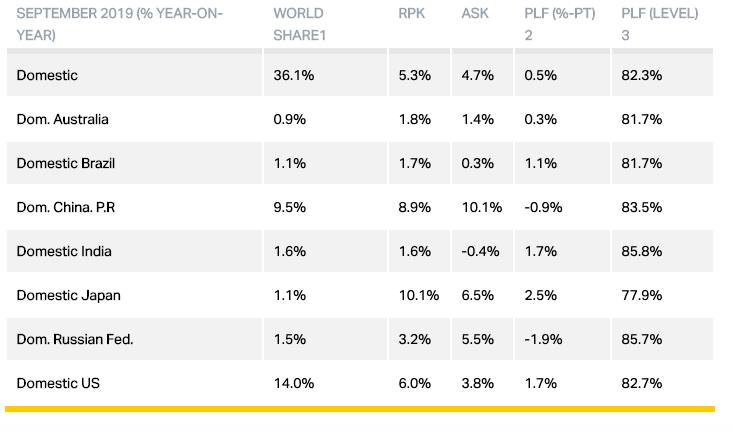

Demand for domestic travel climbed 5.3% in September compared to September 2018, which was an improvement over the 4.7% annual growth recorded in August. Capacity rose 4.7% and load factor increased 0.5 percentage point to 82.3%.

Japanese airlines saw domestic traffic climb 10.1% in September, well up on the 2.0% annual increase recorded in August. However, results are distorted by the weak outcome in September 2018 owing to the disruption caused by Typhoon Jebi.

US airlines’ domestic traffic surged 6.0% in September compared to September 2018, up from 3.9% growth in August year over year. As with Japan, the performance is somewhat exaggerated owing to the softer demand environment experienced in 2018. Nevertheless, the demand environment is robust.

The Bottom Line

«These are challenging days for the global air transport industry. Pressure is coming from many directions. In a matter of weeks, four airlines in Europe went bust. Trade tensions are high and world trade is declining. The IMF recently revised down its GDP growth forecasts for 2019 to 3.0%. If correct, this would be the weakest outcome since 2009, when the world was still struggling with the Global Financial Crisis.

«At times like these, governments should recognize the power of aviation connectivity to ignite the economy and drive job creation. Instead, too many governments—in Europe in particular—are fixated on aviation as the goose that lays the golden eggs of taxes and fees. It’s the wrong approach. Aviation is the business of freedom. Governments should harness its power to drive GDP growth, not tie it down through heavy and punitive tax and regulatory regimes,» said de Juniac.